Designing for NTAP

In the medtech startup world, reimbursement used to be a later-stage conversation. Something you figured out after regulatory approval, once you had clinical data and a commercial team in place. Today, however, reimbursement shows up in the earliest board decks and seed stage conversations. Investors will ask founders about coding, coverage, and payment before a prototype is even complete. Founders are expected to have a view on hospital economics alongside their product development, clinical, and regulatory strategies.

Within that shift, the New Technology Add-On Payment program has taken on outsized importance. It is often framed as a bridge that will make hospital economics work at launch. For many early-stage companies, NTAP is framed as the answer to the question, “How will we get paid at launch?”

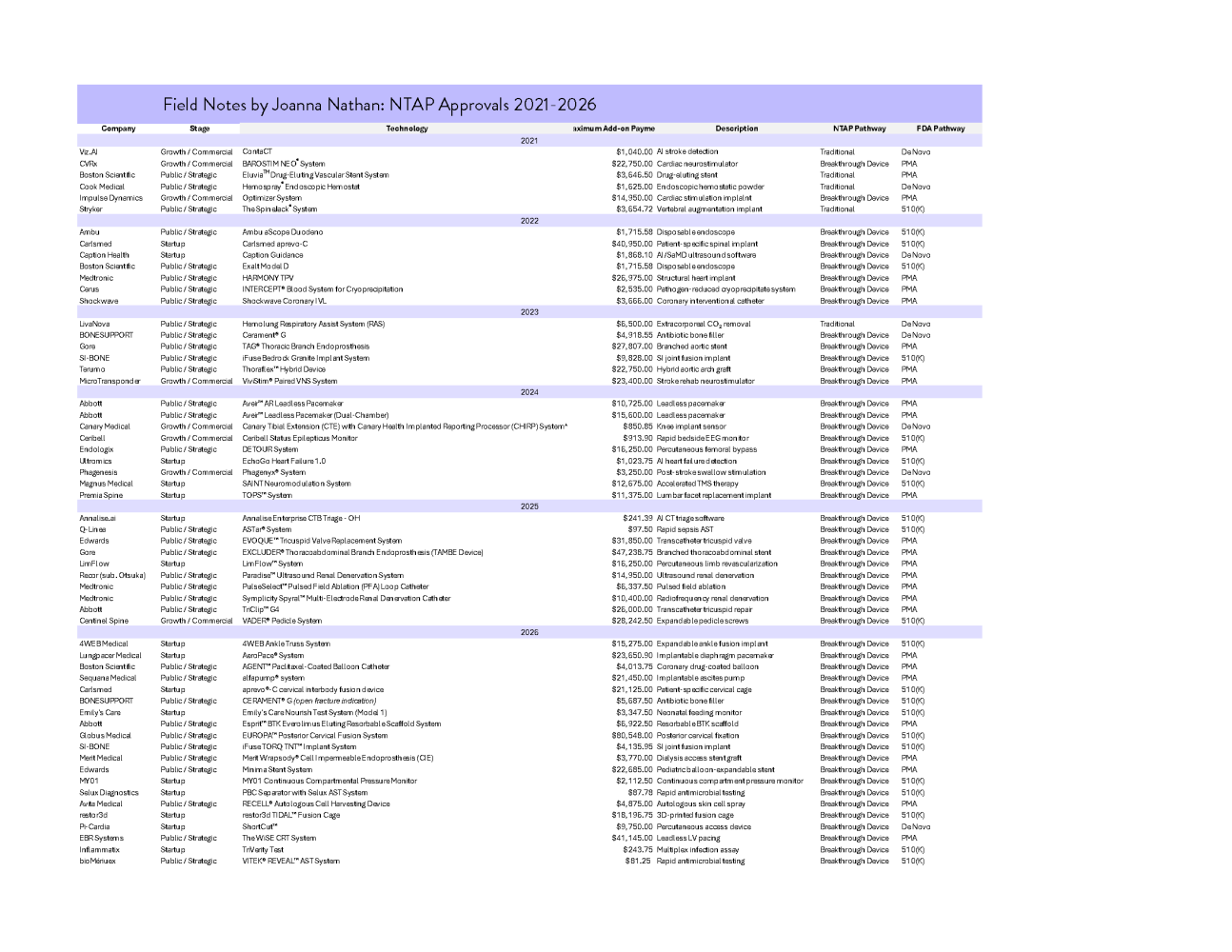

I was curious whether the reality matches the narrative. So I went back and pulled six years of Proposed and Final Rule NTAP data from FY2021 through FY2026. I wanted to see what the actual approval patterns and dollar amounts tell us about who gets awarded NTAP, how often, and in what categories.

NTAP 101

NTAP was established in the early 2000s to address a structural lag in Medicare’s inpatient payment system. Hospitals are paid under fixed Diagnosis-Related Groups, which are recalibrated using historical cost data. When a genuinely new and costly technology enters the market, that cost is not immediately reflected in the DRG rate. NTAP was created as a temporary add-on to reduce that gap. To qualify, a technology must be new, inadequately paid under existing DRGs, and demonstrate substantial clinical improvement. The payment covers a percentage of the excess cost above the DRG payment, up to a capped amount, and typically lasts up to three years before being folded into broader rate updates.

There are two procedural routes into NTAP. Under the Traditional pathway, companies must independently demonstrate newness and substantial clinical improvement to CMS, even if the device is already cleared or approved by the FDA. Under the Breakthrough pathway, devices that receive FDA Breakthrough Device designation are not required to separately demonstrate substantial clinical improvement to CMS in the same way as Traditional applicants. Instead, CMS considers the FDA’s Breakthrough determination as meeting that element of the NTAP criteria. Companies must still demonstrate that the technology is new and that it is inadequately paid under existing DRGs, but the clinical improvement hurdle is effectively streamlined. Over time, that alignment has made Breakthrough designation increasingly relevant not just for regulatory strategy, but for reimbursement positioning as well.

NTAP Has Become the Economic Extension of Breakthrough

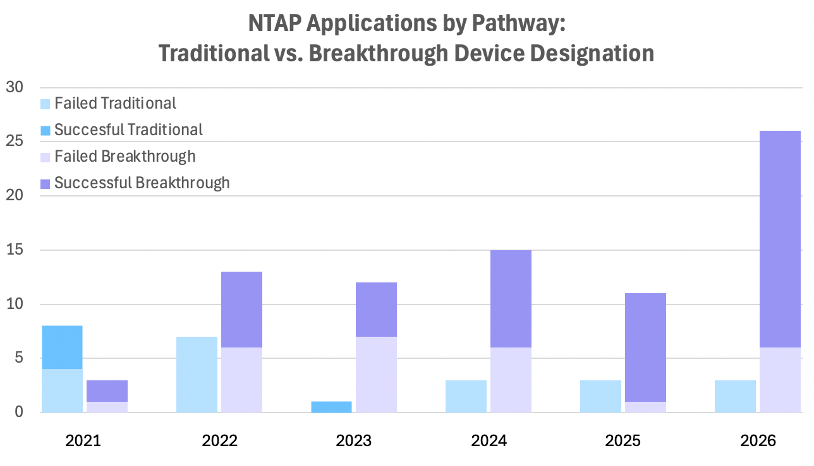

When you step back and look at six years of data, NTAP has become increasingly concentrated around Breakthrough devices. From this dataset, from 2021 through 2026, 76% of applications that made it to the Proposed Rule phase were Breakthrough device, and 91% of the successful awards came from Breakthrough applications. The overall success rate for Breakthrough devices in this sample was 66%. Devices coming through the traditional pathway cleared at 20%. From 2024 through 2026, device applications via the traditional pathway went 0 for 9.

If you are a founder planning your regulatory and reimbursement strategy, this might significantly shift things early on in your company’s life. NTAP is essentially functioning as the reimbursement complement to FDA’s Breakthrough program. The data shows it’s not impossible to succeed through the traditional pathway, it’s just statistically harder, and the gap has widened over time.

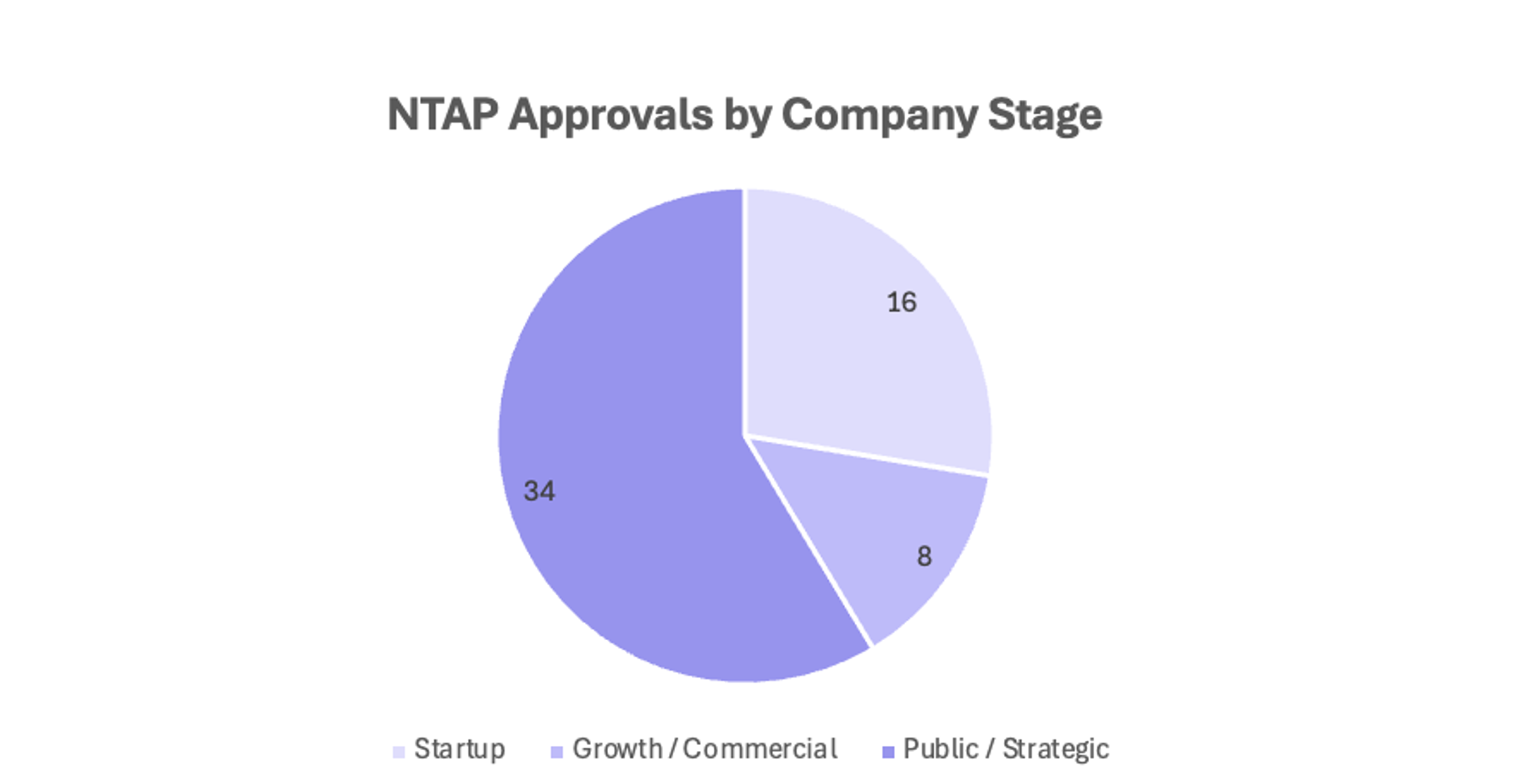

Startups Are Competitive, But Fewer Step Into the Arena

When you look at payment size alone, startups are holding their own. The median NTAP payment for startups in this dataset is $10,562. Growth-stage companies sit at $9,100. Public and strategic players come in at $6,711. The bigger difference is volume. Public and strategic companies account for the majority of NTAP entries in this dataset. Startups represent a smaller portion of the applicant pool. When they do apply, they are competitive on both approval and payment magnitude. In several cases, startup awards sit well above $15,000.

The distribution suggests that NTAP is not structurally biased against early-stage companies. However, fewer startups are submitting, likely because the high bar of clinical evidence, cost data requirements, and timing alignment with FDA clearance are challenging.

Indication Predicts Payment

When you look at NTAP awards by therapeutic area, the payment distribution closely mirrors where capital has concentrated, but with an important distinction. Structural heart, vascular, and spine platforms consistently generate five-figure add-on payments. Neuromodulation also appears in the dataset with significant awards attached. These are capital-intensive technologies with higher per-case costs, which naturally create larger deltas above the DRG and therefore larger NTAP ceilings. This tracks with the reporting in the 2025 HSBC Venture Healthcare Report, which highlights sustained investment strength in neuro, surgical, and cardiovascular categories, particularly in later-stage and large rounds. The same categories attracting substantial venture dollars are often those capable of materially shifting inpatient economics on a per-procedure basis.

AI, imaging, and diagnostic platforms also feature prominently in the HSBC report, particularly in large neuro and imaging financings. In the NTAP dataset, however, many of these awards land in the hundreds or low thousands of dollars. NTAP rewards technologies that materially increase per-case inpatient cost. Many AI and monitoring companies are not designed to do that. Their economic thesis is based on scale and deployment across large populations. For these platforms, NTAP is not the economic engine. It may provide early validation, but the long-term reimbursement strategy rests elsewhere.

PMA Devices Drive the Upper End of NTAP

When you review the data by FDA clearance pathway, it’s clear that PMA devices sit in a different range. In this dataset, PMA devices have a median NTAP payment of $15,925 and an average of $17,285, with maximum awards reaching $47,238. This isn’t surprising, as PMA devices tend to be implantable, higher-cost systems that materially shift the economics of an inpatient stay. Because NTAP is calculated based on excess cost above the DRG, higher-cost devices naturally generate larger add-on payments.

Even though PMA devices dominate the high-payment tier in this dataset, the most interesting nuance is what happens in 510(k). The median 510(k) payment is only $3,501, which tells you most 510(k) awards behave more like De Novo from an economics standpoint. But the pathway has a long tail. The maximum 510(k) award in this sample is $80,548, higher than any PMA award here. That suggests a 510(k) plus Breakthrough combination can still produce a major add-on payment when the device materially changes case cost. It’s possible, but it appears to be the exception rather than the rule. Most non-PMA devices cluster toward the lower end of the payment range.

Takeaways for Founders

Pursuing Breakthrough Device Designation isn’t just regulatory strategy, it is a reimbursement strategy. If NTAP is part of your launch plan, Breakthrough Device Designation materially changes the odds. Traditional pathway success has narrowed, and most successful NTAP awards now run through Breakthrough. Reimbursement positioning begins earlier than many founders think.

NTAP is competitive for startups, but it requires intention. The data does not show structural bias against early-stage companies. Startups that apply are competitive on both approval and payment size. The friction appears earlier in the funnel. NTAP requires aligned regulatory timing, credible cost data, and a clear clinical improvement narrative. It has to be designed into your plan.

NTAP rewards cost displacement, not just innovation. The size of the add-on payment is mechanically tied to how much your device changes the economics of an inpatient stay. High-cost implant systems generate larger deltas. Many other technologies may deliver clinical value without materially shifting DRG math. If your device does not move inpatient cost in a meaningful way, NTAP may validate the story, but it is unlikely to be the economic engine.

For founders who want to look deeper, the annual Proposed and Final Rule determinations are published on the Federal Register, and beginning in FY2024, individual NTAP applications and supporting materials are available through CMS’s MEARIS portal.